Kingsbridge insurance

Sole trader public liability insurance: Comprehensive guide

What can public liability insurance cover do for your business?

It can provide essential protection, offering a safety net against unforeseen circumstances, including third-party injury and property damage claims arising from your business actions.

It helps cover potential financial losses and gives you peace of mind, allowing you to focus on growing your business without worrying about unexpected liabilities.

What are the risks if you DON’T have sole trader insurance?

Without it, you risk significant financial loss, which could jeopardise your business. Even the most careful sole traders can be held liable for accidents, damage, or injuries that happen in connection with their business. The financial costs from compensation claims and legal expenses can be devastating, potentially leading to bankruptcy or business closure.

The risks to sole traders: A case study

John is a sole trader running a small handyman business. He faces a potential lawsuit after accidentally damaging a client’s expensive antique furniture during a repair job. The client is threatening legal action to recover the cost of the damage.

Without public liability insurance, John is worried about the cost of a lawsuit, which could wipe out his savings and potentially bankrupt his business through major legal expenses.

Additionally, negative word-of-mouth and potential bad reviews could tarnish his reputation, making it hard for him to secure future clients and maintain his livelihood.

With public liability insurance, John would have had the sole trader cover to manage these risks, protect his finances, cover the costs, and had the peace of mind needed to focus on growing his own business further.

What does business insurance cover for sole traders?

Sole trader insurance cover protects your business against:

Injuries to third parties

Covers compensation for injuries sustained by clients, customers, or the public due to your business.

Damage to property

Covers costs for repairing or replacing property damaged by your business.

Legal defence costs

Covers expenses for legal representation and court fees if legal claims are made against you.

Product liability

Covers injuries or damage caused by products your business supplies or manufactures.

How much business insurance do sole traders need?

It depends on factors like the size and nature of your business, industry regulations, and contract requirements. Consider the potential risks, and the likelihood of public liability claims. Higher-risk industries may require additional cover.

Industry standards and client contracts often seek minimum coverage levels. Assess your business operations and potential liabilities carefully to work out the right level of cover for you.

It’s a good idea to talk to an insurance provider like Kingsbridge to tailor your cover to your specific needs, making sure you’re adequately protected against potential financial risks associated with third-party injury or property damage claims.

Get the right level of insurance cover with Kingsbridge

At Kingsbridge, we offer personalised consultations to work out the appropriate level of cover for you, considering industry standards, regulatory requirements, and potential liabilities, giving you comprehensive protection tailored to your needs.

How to choose the right public liability insurance

Get quotes

Research insurers online or through referrals. Give accurate details about your business activities when asking for quotes.

Compare insurance policies

Look beyond price. Compare cover limits, exclusions (e.g., hazardous activities), and excess amounts.

Check out our guide on how to compare insurance quotes fairly for some top tips.

Choose an insurance provider

Consider insurer reputation, customer reviews, and claims handling. Make sure they specialise in sole trader needs.

Review policy

Check for adequate cover limits matching industry standards. Understand exclusions, such as deliberate acts or contract disputes.

Consult

Seek advice from insurance experts like Kingsbridge for personalised guidance on choosing the best policy for your specific business risks and budget.

At Kingsbridge, we specialise in sole trader public liability insurance, and we’ve got the expertise and professional services you need to help you find the best deals. We’re a trusted expert in sole trader insurance, ensuring cover against potential legal costs and compensation claims.

Additional cover with Kingsbridge insurance

Accidents happen. With Kingsbridge, you’ll benefit from additional insurance coverage for complete protection, safeguarding your business against various risks and providing peace of mind. This cover includes:

Professional Indemnity: Covers legal costs and damages caused by compensation pay outs if you provide negligent advice or services, resulting in client loss.

Employers’ Liability: Mandatory if you have employees, covering claims from staff injured or falling ill due to their work.

Occupational Personal Accident: Provides income replacement if you are unable to work due to accidental injury, ensuring you don’t lose money.

Tools and Equipment: Protects against loss or damage to essential tools and equipment used in your business.

As expert insurance providers, we’ll also provide you with the professional advice you need.

While reputational damage isn’t directly covered by public liability insurance, Kingsbridge’s Professional Indemnity Insurance can offer an extra layer of protection against claims of negligence that could harm your business’s standing.

Ready to get covered? Get your personalised quote now and safeguard your business today.

How to make an insurance claim

Notify your insurer

Inform your insurer about the incident as soon as possible.

Gather documentation

Provide necessary documentation, such as photos, witness statements, and any correspondence related to the claim.

Insurance assessment

Your insurer will assess your claim, potentially sending an adjuster to investigate.

Determination and compensation

Once reviewed, your insurer will determine cover and manage the compensation process.

At Kingsbridge, we support sole traders by offering expert guidance throughout this process. We’ll help you with documentation, provide legal advice, and ensure timely communication with all parties involved, helping to streamline the claims process and minimise any stress for you.

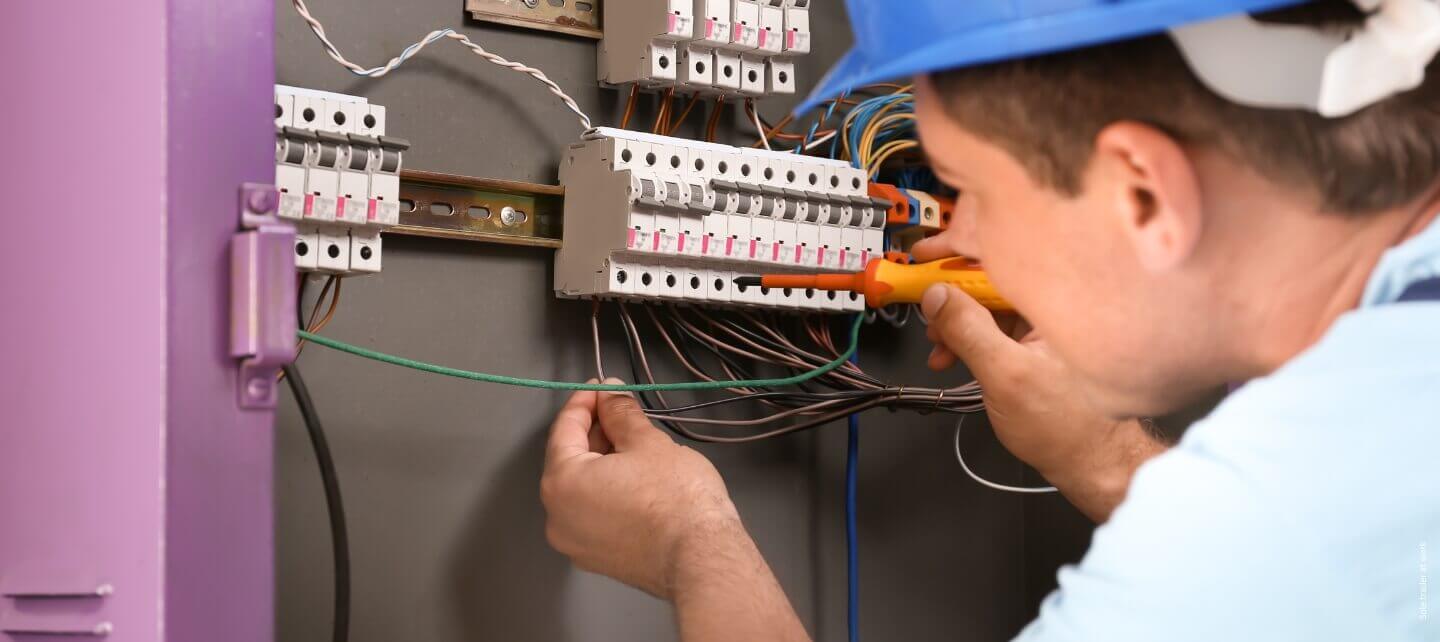

Why business insurance is important for builders

Builders face unique risks in their profession due to the nature of their work, which often involves operating in environments where there is a high potential for accidents and damage. Here are some key reasons why it is particularly crucial for builders:

High risk of injury

Construction sites are inherently hazardous. There is always a risk that a member of the public could get injured, whether by falling debris, tripping over equipment, or being struck by tools. Insurance covers the legal costs and compensation claims that can arise from such incidents.

Property damage

Builders frequently work on or near other properties. Accidental damage, such as a hammer breaking a window or heavy equipment damaging landscaping, is a common risk. Insurance makes sure that the costs of repairs or replacements are covered, protecting builders from substantial financial liabilities.

Client and contract requirements

Many clients and contractors require proof of public liability insurance before they will hire a builder. Having this insurance in place not only helps secure contracts but also demonstrates professionalism and reliability.

Legal defence costs

If a claim is made against a builder, legal defence costs can be significant. Insurance covers these expenses, ensuring that builders can afford quality legal representation without suffering financial loss.

Reputation management

An accident or incident causing damage can harm a builder’s reputation, making it difficult to secure future work. Insurance helps manage these situations by covering costs and allowing builders to address issues promptly and effectively.

How public liability cover helps: A case study

Consider a real-world scenario where a builder, John, was renovating a client’s home. During the renovation, a ladder accidentally fell, injuring a neighbour who was visiting the site. The neighbour required medical treatment and subsequently filed a compensation claim for their injuries.

Without insurance, John would have faced significant medical expenses, and potential compensation payments, threatening his financial stability and business continuity.

However, because John had public liability insurance, his insurer covered the medical costs and legal fees, and the compensation was handled without a significant financial burden on John. This allowed him to continue his business operations without interruption and maintain his reputation as a reliable and responsible builder.

How to make an insurance claim with Kingsbridge

Notify your insurer

As soon as an incident occurs, notify Kingsbridge immediately. This will make sure that the claims process can start without delay.

Gather documentation

Collect all necessary documentation, such as photographs of the incident, witness statements, and any correspondence related to the claim.

Assessment

Kingsbridge will assess your claim, which may include sending an adjuster to investigate the incident and gather further details.

Determination and compensation

Once the assessment is complete, Kingsbridge will determine cover and manage the compensation process, keeping you informed throughout.

Kingsbridge supports sole traders by offering expert guidance throughout the claims process, helping with documentation, providing legal advice, and ensuring timely communication with all parties involved. This support helps streamline the claims process and minimises stress for you.

Tips for choosing the right business insurance

When choosing the right sole traders insurance cover options for your sole trader business, consider the following tips:

Understand your risks

Assess the specific risks associated with your business activities. This helps determine the necessary cover limits and policy specifics.

Compare insurance policies

Don’t just focus on price. Compare different policies for cover limits, exclusions, and excess amounts. Look for comprehensive coverage that suits your needs.

Check insurer reputation

Choose an insurer with a good reputation. Read customer reviews and check their claims handling process to ensure reliability.

Review insurance policy details

Make sure the policy provides adequate cover for your industry standards. Understand all exclusions and make sure they don’t leave you exposed to significant risks.

Seek expert advice

Consult with insurance experts like Kingsbridge for personalised guidance on choosing the best policy for your specific business risks and budget.

Business insurance: In summary

You’ve invested a lot of time, energy, and money building your own business. Don’t risk it. Secure it with public liability insurance today.

FAQs – Common questions about public liability insurance

How much does insurance typically cost for a sole trader?

The cost varies, depending on your profession, location, and the level of cover you choose. However, you can find policies starting from as low as £150 per year. It’s always best to compare quotes to find the best deal.

What are the main benefits of having insurance as a sole trader?

It protects your business from the financial impact of claims made by the public for injury or damage to someone’s property, covering legal fees and compensation pay outs. Also, it gives you peace of mind and can enhance your professional reputation.

Are there any specific industries where insurance is more crucial?

Yes, it is particularly important for sole traders who work directly with the public or on their premises, such as tradespeople, cleaners, and therapists. However, it’s beneficial for any sole trader as accidents can happen unexpectedly.

Will it cover both my business and personal finances?

It primarily covers your business assets. However, as a sole trader, your personal assets may also be at risk if your business is sued. It’s important to discuss your specific needs with Kingsbridge to ensure adequate protection.

How quickly can I get public liability insurance cover after signing up?

In most cases, you can get cover almost instantly after buying a policy online. You’ll typically receive your policy documents via email, providing immediate proof of insurance.

Do tradesmen need to have it?

While it isn’t legally required for most sole traders, including tradesmen, it is highly recommended. Many clients and contractors require proof of public liability insurance before hiring a tradesperson.

What business insurance do I need if I’m a self-employed professional?

The type of insurance you need depends on your specific business activities and risks. However, public liability insurance is often considered essential for most self-employed individuals. Other types of insurance you might consider include professional indemnity, business equipment cover, and personal accident insurance.